Hello. This is Stanton Jones with what’s important in the IT and business services industry this week.

If someone forwarded you this briefing, consider subscribing here.

What You Need to Know

Signals indicate that enterprises are consolidating a significant share of their managed services spend with fewer providers. What does that mean for IT and business services in the second half of 2026?

Data Watch

Background

As we discussed on the 1Q26 ISG Index call, the managed services market was steady in the first quarter, generating just over $11 billion of annual contract value (ACV), up 3% Y/Y. While overall growth was muted, when you look inside the number, you can see an interesting story.

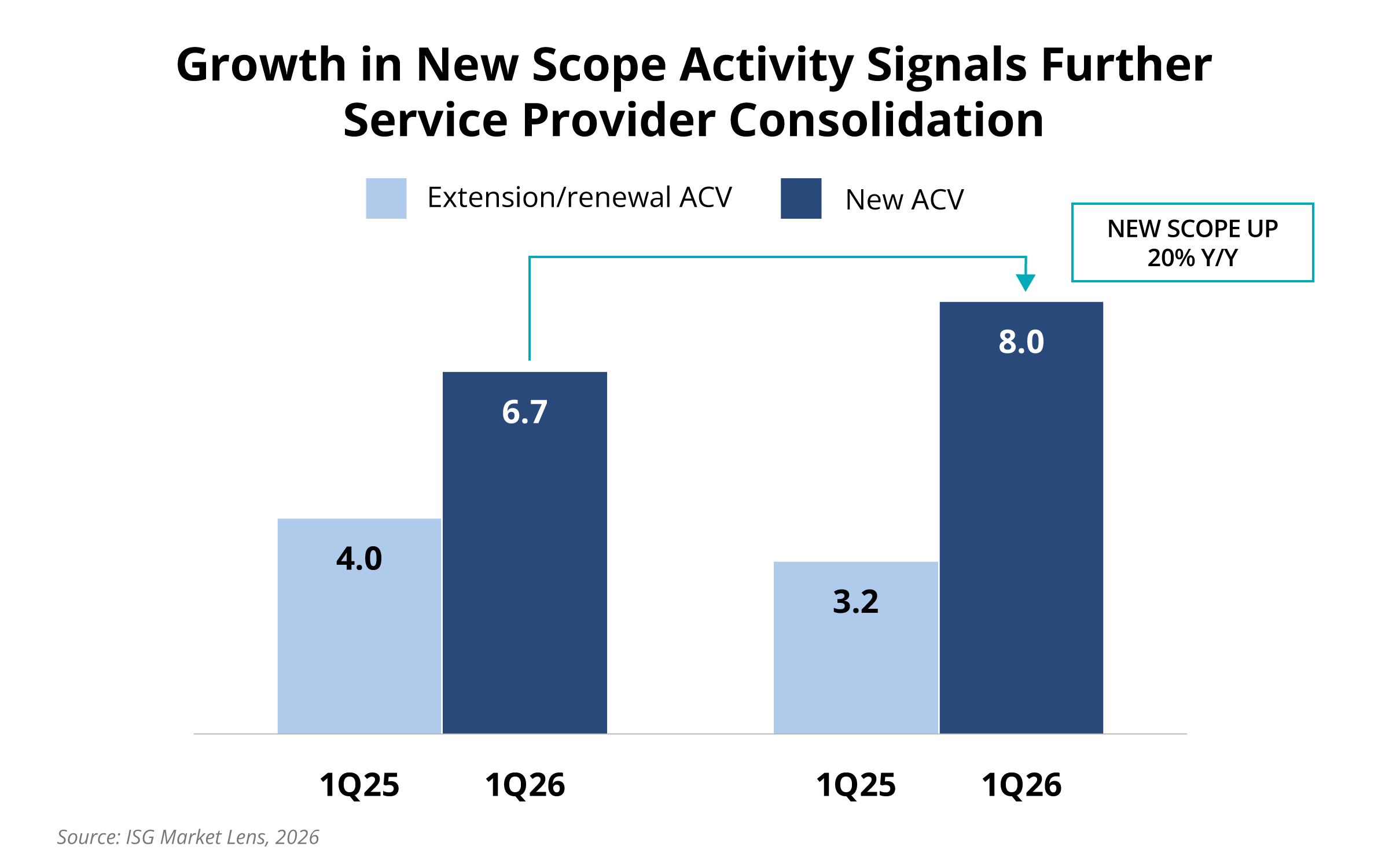

New scope ACV was up 20% and had its best quarter ever (see Data Watch).

However, there is an important qualification on what we mean by “new” scope. We’re looking at this through the lens of a service provider, so if the award is not an extension or a renewal, it’s considered new scope. So in this case, wallet-share shifts represent new work for the provider winning the business.

This means that when there’s an increase in new scope ACV during a time when overall spending is mostly flat (like today), it’s a likely indicator of provider consolidation. We’ve discussed the other signals of provider consolidation from an enterprise lens here in 2025 and again earlier this year.

The Details

- New scope ACV in 1Q26 of $8 billion was up 20% Y/Y.

- On the other hand, renewal and extension ACV of $3.2 billion was down 24% Y/Y.

The Incumbents’ Disadvantage?

So, the question then becomes: Are enterprises moving away from their incumbent providers?

In some ways you could argue that incumbency has actually become a disadvantage in this market. Enterprises are aggressively taking scope to the market and are going competitive to drive savings. As we noted in some earlier research, over 60% of enterprises are consolidating providers to reduce costs.

In our view, it’s consolidation that is driving much of this new scope. Account incumbents, who already have visibility into the landscape but don’t yet own a significant share of the TCV, are actively shaping deals at the executive and board level. When they win, adjacent scope often gets rolled up into a much larger transaction, often lasting five, seven or even 10 years. This is why, in today’s market, it can actually be a disadvantage to be a large incumbent.

This trend is likely to continue through the rest of the year as providers continue to compete aggressively to gain wallet share in a low single-digit growth environment.

About the author

Stanton Jones

Stanton helps enterprise technology leaders, IT service providers and buy- and sell-side professionals make sense of the global IT services sector. Stanton's weekly briefing - the Index Insider - is read by thousands of industry stakeholders each week.